BUSINESS NEWS

Wall Street sees elevated recession risk amid US-China trade fight

[ad_1]

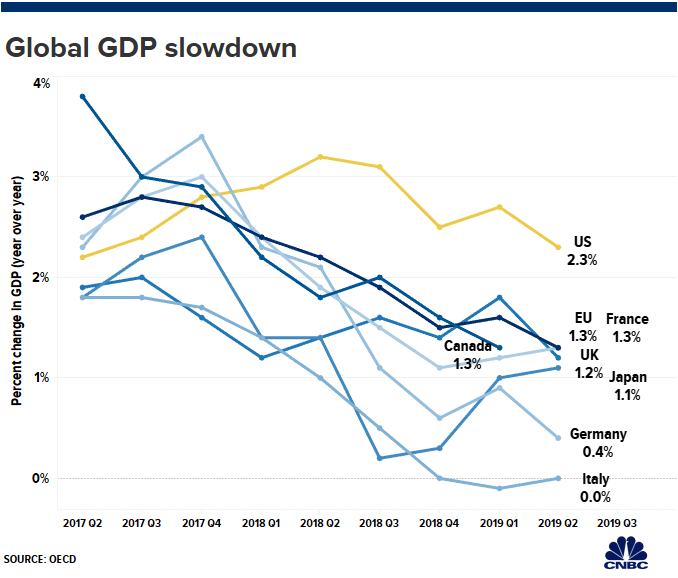

The reignited trade fight between the U.S. and China elevates the odds of a global recession and market pullback over the next year, according to some of Wall Street’s top economists and market strategists.

The global economy would fall into recession six to nine months after the U.S. and China enforce their new round of tariffs, wrote Morgan Stanley’s chief economist, Chetan Ahya.

“Risks remain skewed towards further escalation at least until material market or economic weakness shows,” Ahya told clients in a note. “Continued trade tensions, combined with reactive monetary and fiscal policy, mean that the risk of non-linear tightening in financial conditions, triggering a global recession, is high and rising.”

Angst over the back-and-forth tariff battle between the U.S. and China has been a major driver of business sentiment, with executives expressing concern in earnings calls and surveys alike. But those fears can also have more material impact when C-suite leaders choose to postpone capital investments like the construction of new factories out of fear of supply chain disruption or the imposition of import duties.

Stocks rose Monday following a Friday swoon after President Donald Trump stoked trade tensions, a move that sent the Dow down 623 points. The president, in a series of tweets, ordered American companies “to immediately start looking for an alternative to China” and asked “who is our bigger enemy, [Federal Reserve Chairman] Jay Powell or Chairman Xi?”

The trade anxieties peaked following the market’s close, when Trump announced that the U.S. would respond to China’s trade countermeasures by raising tariffs on $250 billion worth of Chinese goods to 30% from 25%. Tariffs on another $300 billion in Chinese products will also go up to 15% from 10%, he said.

For his part, Ahya believes the revelation that the trade fight may last far longer could depress corporate sentiment even further.

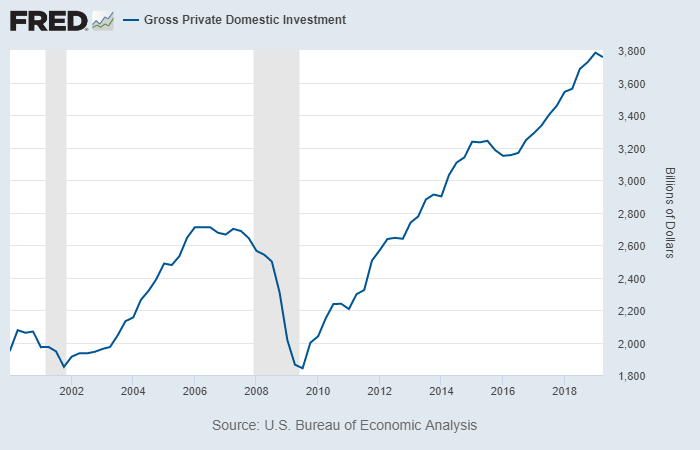

Those concerns manifested in the most recent U.S. GDP report. Gross private domestic investment tumbled 5.5% in the second quarter, the worst since the fourth quarter of 2015 as spending on structures slumped 10.6%. The decline pulled a full percentage point from the final GDP number of 2.1%.

The souring global outlook is bad enough to warrant a portfolio shift, wrote Mark Haefele, global chief investment officer at UBS Wealth Management.

“With talks between the US and China dominating market moves over the near term, investors should brace for higher volatility. We believe it is prudent to take action to neutralize part of this event risk,” he wrote. “As a result, we are reducing risk in our portfolios by moving to an underweight in equities to lower our exposure to political uncertainty.”

Haefele added that while action by the Federal Reserve can minimize downside, he’s no longer confident the central bank is capable of pushing stocks higher. Instead, UBS continues to recommend investors look for opportunities in carry strategies in credit and foreign exchange markets, which stand to benefit from a worldwide shift by central banks to easier monetary policy.

“We continue to take risk on income-enhancing strategies, which benefit from central bank easing as global growth slows,” he wrote. “This includes overweight positions to European investment grade bonds and … an overweight to US dollar-denominated emerging market sovereign bonds.”

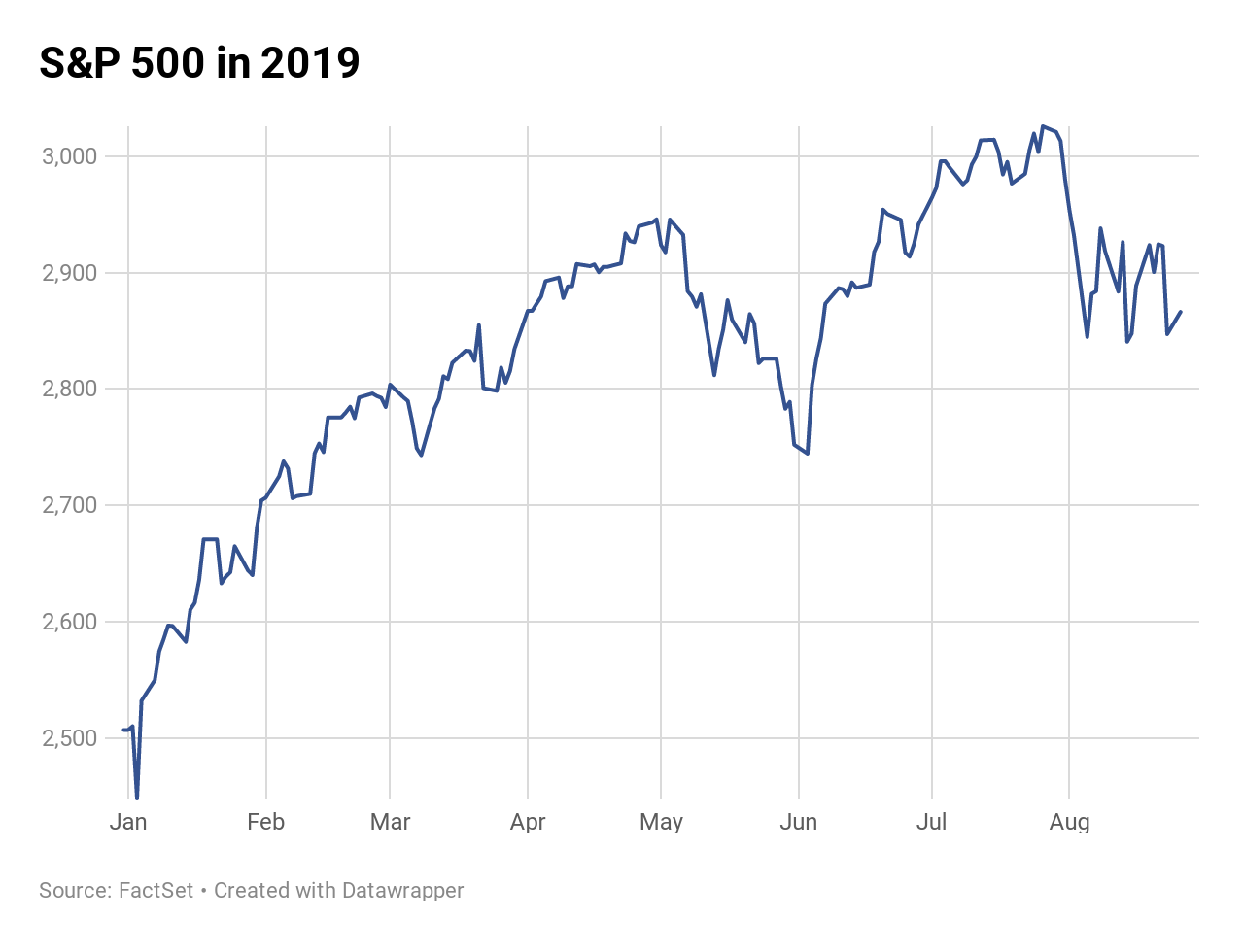

Despite the overarching gloom and doom, some market watchers are taking the recent volatility in stride and point out that U.S. stocks remain on track to post impressive gains in 2019.

“Yes, these scary headlines and 3% drops on one tweet obviously aggravate everyone. But in the bigger perspective of things, things are positive,” Ryan Detrick, senior market strategist at LPL Financial, told CNBC’s “Squawk Box ” on Monday morning.

August and September are known as historically turbulent months for the market, and by some metrics, even appear to be less turbulent than usual, the strategist said.

“The most the S&P has pulled back this year is 7%; the average year pulls back about 10%,” he added. “We’ve had two separate, 5% corrections; the average year sees four.”

The S&P 500, which dropped nearly 1.5% last week, has only once posted a five-week losing streak since the current bull market began a decade ago, the strategist said, adding that the longer uptrend “is still good.”

To be sure, despite a volatile August, the 500-stock index is still up more than 14% year to date, on track for its fourth-best calendar year since the financial crisis. The Nasdaq Composite, S&P 500 and Dow all remain within a few percent of their respective record highs.

“Fifteen years ago today was my first date with my wife,” Detrick said. “Anyone who’s been in a 15-year relationship will tell you there’s ups and downs.”

How the market ultimately ends 2019 will almost certainly depend more on what Washington and Beijing do as opposed to what they threaten. But it will also hinge on 2020 earnings growth expectations and price levels, said RBC Capital’s head of equity strategy, Lori Calvasina.

“If positioning, valuation, and trade rhetoric don’t improve by the time the S&P 500 reaches 2725, we could easily see the decline in the US equity markets totaling 10-20% from the late July high,” she wrote. “While our base case has been for a pullback of around 10% in the months ahead, we do believe the risk of a growth scare taking hold of the US equity market is rising rapidly.”

Calvasina sees the S&P 500 ending the year at 2,950, about 3.5% above Friday’s close.

[ad_2]

Source link